Quarterly Market Performance Commentary

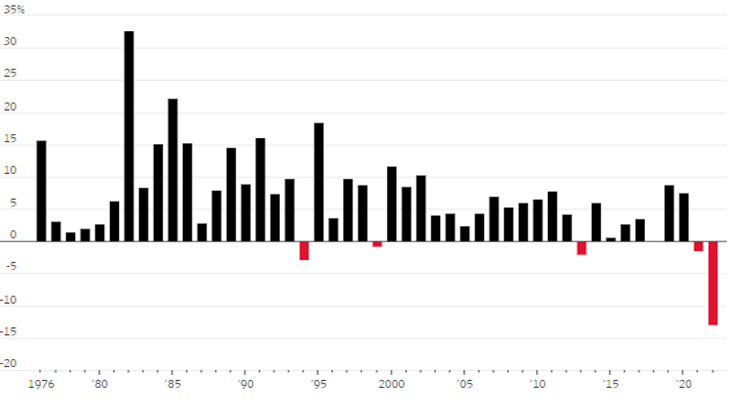

The fourth quarter of 2022 completed a tumultuous financial year with moderately better results than were observed in prior quarters. Although no substantial gains occurred, major indices (DJIA, NASDAQ, S&P 500, and Russell 2000) saw relatively stable results throughout the quarter. However, looking at the financial year as a whole, 2022 was riddled with poor performance as a prolonged volatile bear market took hold and prospects of a recession loom into 2023. Excluding the DJIA, most other major indices saw double-digit losses throughout the year. Furthermore, bonds, which typically are viewed as a safe-haven investment, delivered unprecedented losses. The Bloomberg U.S. Aggregate Bond Index, an index measuring the investment-grade bond market, returned -13.01%, which is by far the worst calendar year performance since the index’s inception in 1976 (See Figure 1 below).1 This poor performance is primarily due to the inverse relationship between bond prices and interest rates. The U.S. Federal Reserve sought to combat stubborn inflation by increasing interest rates at an unprecedented rate, thus driving down bond values. Outside of traditional investments, other securities such as Special Purpose Acquisition Companies (SPACs), Crypto, and NFTs have also plummeted in value. Many investors are reevaluating their portfolios as the fear of a looming recession has increased.2

Figure 1: Bloomberg U.S. Aggregate Bond Index Total Return

Figure 1. Source: Goldfarb, Sam. “For Battered Bonds, Threats of Further Losses Linger” The Wall Street Journal, https://www.wsj.com/articles/for-battered-bonds-threats-of-further-losses-linger-11672602373?mod=Searchresults_pos2&page=1The global markets were impacted in a number of ways in 2022. Some of the main themes include supply chain issues that prevailed throughout the year, the lingering effects of the Covid-19 pandemic, and the ongoing conflict between Russia and Ukraine. Another significant contributor to market performance during the year, as previously mentioned, was the change in the Federal Reserve’s monetary policy to combat high inflation. Most recently, the Federal Reserve increased the federal funds rate by 50 basis points in December, which marked the 7th consecutive interest rate hike of 2022. This most recent increase set rates in the range of 4.25%-4.5%, the highest it has been since December 2007. While the effect that rising interest rates are having on the financial markets is not ideal, 2022’s inflation rates have resulted in a serious increase in living costs, which hope to be stopped through this monetary policy. It appears that this policy has started to show some success in quelling inflation, as the year-over-year Consumer Price Index dropped from 9.1% in June to 7.1% in November.3 Central banks of Europe and England have also adopted a similar strategy to counter inflation, although they have yet to see comparable results.

Despite many economic indicators pointing towards a recession, employment metrics remain stable. The November labor report, issued by the U.S. Bureau of Labor Statistics, showed another month of unexpectedly high hiring and wage increases. The report notes that total nonfarm payroll employment increased by 263,000 during the month, and the unemployment rate remained unchanged at 3.7%. (See Figure 2 right).4 Jerome Powell believes if companies were to reduce the number of job openings and did not perform staff cuts, this would aid in reducing inflationary pressures. Despite this, the number of new hires remains fairly stable – the relative strength of the labor market can be seen as a good sign for the economy but may cause the Federal Reserve to continue its tightening of monetary policy into 2023. “November’s labor market report was clearly bad news for the Fed’s war on inflation,” said Jan Groen, Chief U.S. Macro Strategist at TD Securities in New York.5

Figure 2: Unemployment Rate, Seasonally Adjusted

Experts are not certain this strong labor market will continue throughout 2023. Many small businesses and certain sectors such as leisure and hospitality are still eager for new employees, while large companies and other sectors appear over-saturated. This is especially seen with technology companies; Twitter, Amazon and Meta having all experienced large job cuts this year. “The labor market might encounter some bumps in the road next year, but it’s heading into 2023 cruising,” said Nick Bunker, head of economic research at the Indeed Hiring Lab.5

Figure 2 Source: “The Employment Situation – December 2022” Bureau of Labor Statistics, 2 December. 2022, https://www.bls.gov/news.release/empsit.nr0.htmLegislative Update – SECURE 2.0 Passed

The much anticipated Securing a Strong Retirement Act of 2022 (“SECURE 2.0”), included in the $1.7 trillion omnibus spending package, was signed into law by President Biden on the 29th of December. This Act was the culmination of three bills – the Senate’s EARN Act, and RISE and SHINE Act, along with the House of Representatives’ SECURE 2.0 Act, which all had similar goals of improving the United State’s Retirement System.6 The act marks the second round of major retirement reform since the passage of the Setting Every Community Up for Retirement Enhancement Act (“SECURE Act”) which was signed into law in December 2019.

Nearly 400 pages in length including 90+ new retirement plan provisions, it goes without saying that SECURE 2.0 is a wide-reaching piece of legislation that will impact many areas within the retirement system.7 The timeline to roll out each provision, and whether the provision is mandatory, varies amongst each section. Figure 3 to the right illustrates 10 of the key provisions included within the legislation. Keep in mind that this list only scratches the surface of SECURE 2.0 and many updates will follow as the industry considers all implications of the new legislation.

SECURE 2.0 has generally been viewed positively by players in the retirement industry, as it will allow for the expansion of benefits to both plan sponsors and employees.8 Among many other items, plan sponsors will see improvements such as added flexibility in making beneficial retirement plan amendments, allowing for “excludable employees” during top-heavy testing, and increasing the maximum mandatory distribution, also known as plan force-outs, limit to $7,000 (from $5,000). Employees, on the other hand, will be granted many benefits that increase retirement plan flexibility, such as delayed required minimum distributions, the ability for student loan matching (based on employer elections), and additional catch-up contributions for those between the ages of 60 and 63.

Another welcome change that will soon be required by SECURE 2.0 is the creation of a searchable online database of lost retirement accounts. In theory, this will allow for individuals to easily search and locate lost retirement plan assets that exist in prior employer plans—an issue that has plagued the industry for years. Beginning in 2025, retirement plans will be required to share information with the Department of Labor to be included in the database.

Any applicable updates to plan documents that result from SECURE 2.0 will be handled by your recordkeeper or third-party administrator. Keep an eye out for further communication from Forest Capital Management or your other retirement plan service providers for updates pertaining to this new legislation.

Figure 3: SECURE 2.0 – 10 Key Provisions

Auto-enrollment and escalation: New 401(k) and 403(b) plans would have to start enrolling participants with a salary deferral of at least 3% of salary, no higher than 10%, and escalate at 1% per year of service up to a minimum of 10% and a maximum of 15%. An employee can opt out of the auto-enrollment and escalation. Small businesses, new businesses, and church and government plans are exempted from this provision.

Required Minimum Distributions: The age for required minimum distributions is 72. It would be increased to 73 in 2023 and 75 in 2033.

Student Loan Matching: Starting in 2024, employers could match student loan payments with plan contributions. The provision would not be limited to government debt and could be applied to any loan taken for higher education expenses.

Lost and Found: The Department of Labor would have two years to create an online database of plans so that employees and employers could find missing retirement accounts and match them to their corresponding sponsor and participant.

Auto-portability: A plan provider could transfer a participant’s retirement savings from a previous employer to their new one, unless the participant elects otherwise.

Part-time Employees: Long-term part-timers would have to be enrolled in their employer’s 401(k) after two years, instead of the current timeframe of three years.

Catch-up Contributions: For those aged 60 through 63, catch-up contribution maximums would be increased to $10,000 or 150% of the regular catch-up amount for those aged 50 and older, whichever is greater.

Emergency Savings: Participants would be permitted to withdraw up to $1,000 in one withdrawal per year without an early-withdrawal tax penalty. They would have the option to repay this amount in three years and could not withdraw in this fashion again for three years unless the earlier withdrawal has been repaid. Employers could also offer a retirement plan-linked emergency savings account that would allow four penalty-free withdrawals per year. Employees could contribute a maximum of $2,500 to such an account.

Hardship Withdrawals: Participants could withdraw up to $22,000 to pay for expenses related to a natural disaster, which would be taxed as gross income over three years without additional penalty. Survivors of domestic abuse could also withdraw the lesser of $10,000 or 50% of their retirement account without penalty upon self-certifying as a survivor of domestic abuse.

Increased tax credits for low-income savers: Starting in 2027, low-income savers could receive a tax credit of 50% of their retirement contributions, up to $2,000.

Figure 3. Source: Paul Mulholland, “SECURE 2.0 Bill Delivers on Most Supported Provisions” PLANSPONSOR, 20 Dec. 2022—https://www.plansponsor.com/secure-2-0-bill-delivers-supported-provisions/

コメント